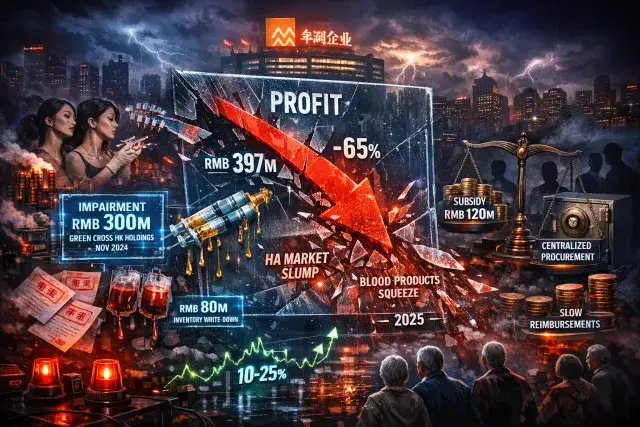

China Resources Boya Bio-pharmaceutical, a key player in blood products and medical aesthetics, has sounded alarm bells with a stark profit warning for 2025. Expecting net profit attributable to shareholders at RMB105 million to RMB136.5 million—down over 65% from RMB397 million last year—this forecast reveals deepening challenges in China's biopharma sector, signaling broader pressures on profitability amid aggressive healthcare reforms.

Key Financial Projections and Impairments

The company's outlook strips away optimism from its recent acquisition, projecting an underlying net loss of RMB7.5 million to RMB15 million after excluding non-recurring gains. Operating revenue should still climb 10% to 25%, fueled by the November 2024 purchase of Green Cross HK Holdings, which bolsters its hyaluronic acid (HA) portfolio. Yet, this growth masks brutal hits:

- RMB300 million in impairments on franchise rights and goodwill tied to the Green Cross deal, triggered by a slumping HA medical aesthetics market.

- RMB80 million drag from inventory revaluation, plus elevated depreciation and amortization.

- Non-recurring items like government subsidies and investment income, totaling around RMB120 million, offer partial relief.

Root Causes: Aesthetics Downturn and Blood Products Squeeze

Management pins the profit plunge primarily on the cooling HA medical aesthetics sector, where demand has softened amid regulatory scrutiny and shifting consumer preferences in China. Once a high-growth area driven by beauty trends, the market now faces overcapacity and price erosion, forcing write-downs on recent investments like Green Cross. Meanwhile, CR Boya's core blood products business grapples with relentless headwinds from Beijing's healthcare policies:

- Centralized procurement and volume-based pricing, compressing margins.

- Payment reforms and stricter medical insurance controls, delaying reimbursements.

- Intensifying competition, eroding pricing power in plasma-derived therapies.

These factors echo industry-wide margin erosion, where gross profits have shrunk as reforms prioritize affordability over premiums.

Implications for CR Boya and China's Biopharma Landscape

This warning underscores operational vulnerabilities for CR Boya and its parent, China Resources Pharmaceutical, highlighting the risks of expansion into volatile aesthetics amid maturing blood products markets. Looking ahead, sustained reforms could further challenge profitability unless offset by cost efficiencies or new revenue streams like innovative biologics. For investors, it signals caution: while revenue growth persists, true earnings power hinges on navigating policy shifts and market cycles. In a sector pivotal to China's aging population and public health, such tremors may prompt a strategic pivot toward resilient, high-barrier therapies.